South Korean Industries Confront Escalating Carbon Challenges

As carbon regulations tighten worldwide, South Korean enterprises are grappling with mounting carbon risks throughout their supply chains. These challenges are intensified by new global directives such as the International Financial Reporting Standards Sustainability Standards (IFRS S2) and the European Union’s (EU) Carbon Border Adjustment Mechanism (CBAM), coupled with voluntary carbon management efforts in the global tech sector.

Emerging markets in Asia, including Singapore and Hong Kong, have implemented IFRS S2, compelling companies to report climate-related risks and opportunities. This includes Scope 1 and 2 greenhouse gas (GHG) emissions beginning with the 2024–2025 reporting cycle, with Scope 3 to follow in 2026.

Scope 1 emissions are directly linked to the production process and are controlled by the company. Scope 2 emissions are indirect, resulting from the purchase of energy used in production. Scope 3 emissions account for the embedded carbon from Scope 1 and 2 activities necessary for producing finished goods. The inclusion of these indirect emissions could significantly amplify supply chain carbon risks, such as:

Investment Aversion

Higher Carbon Cost Exposure

Counterparty and Reputational Risks

The Institute for Energy Economics and Financial Analysis (IEEFA) reports that Samsung Device Solutions, a leading South Korean chipmaker, recorded Scope 1–3 emissions of approximately 41 million metric tonnes of CO2 equivalent (MtCO2e) in 2024. This figure marks the highest among seven major global tech firms, reflecting a carbon intensity of about 539 tCO2e per USD million in revenue. By comparison, SK Hynix, another South Korean chip manufacturer, exhibited a carbon intensity of around 246 tCO2e/USD million.

These emission levels pale in comparison to global tech giants like Apple and Amazon Web Services (AWS), which boast carbon intensities of 37 and 107 tCO2e/USD million of revenue, respectively. These lower figures highlight their strategic commitment to maximizing clean energy sales and reducing GHG intensity.

Investors are increasingly excluding carbon-heavy companies from their portfolios, potentially restricting financing access for high emitters. This exclusion could elevate the cost of capital and diminish corporate valuations due to carbon penalties.

Including indirect emissions in financial disclosures may escalate carbon costs through various regulations, including carbon taxes and ETS compliance. IEEFA’s analysis suggests that if Scope 2 and 3 are incorporated into South Korea’s ETS, Samsung Device Solutions could face carbon costs of approximately USD26 million under the current 10% paid allocation system. This cost could surge tenfold to USD264 million if the free ETS allowance is abolished, and companies must cover 100% of their credit allocations.

Expanding carbon emission disclosures could also heighten counterparty and reputational risks. Companies might shy away from engaging with high-emission firms due to stricter Scope 1–3 reporting requirements, impacting carbon accounting across entire supply chains. High-emission companies risk exclusion from global supply chains as large tech firms like Apple and TSMC endorse carbon reduction initiatives.

The CBAM poses additional carbon risks due to disparities between the EU ETS and South Korea’s ETS, potential adoption by more countries, and possible expansion to cover additional goods. These factors could jeopardize South Korea’s export competitiveness by increasing CBAM financial exposure and encouraging supplier substitutions.

Although semiconductors are currently exempt, an expansion of the EU CBAM to include the sector and indirect emissions could disadvantage South Korean exporters in global trade. IEEFA estimates that if semiconductors fall under the EU CBAM scope, Korean chip importers in the EU might incur approximately USD588 million (KRW847 billion) in CBAM certificate expenses from 2026 to 2034. The increased costs may drive European importers to seek low-emission suppliers to mitigate financial exposure.

South Korea’s economy, heavily reliant on international trade, faces significant impacts due to heightened supply chain carbon risks, which account for about 70% of its GDP. Rising carbon costs in LNG-powered semiconductor clusters and fossil fuel-based AI data centers could exacerbate counterparty risks and escalate production expenses.

To counter these challenges, the South Korean government is advocating for RE100 industrial complexes and developing an ‘Energy Highway’ to enhance renewable energy usage across industries. The ‘Special Act on the Creation and Support of RE100 Industrial Complexes and Energy New Cities’ is expected to be enacted in 2025. The Energy Highway plan includes building a high-voltage direct current (HVDC) transmission infrastructure to link renewable energy-rich areas with consumers.

As global carbon regulations tighten from 2026 amid an uncertain economic landscape, South Korea’s supply chains face exacerbated carbon risks. High tariffs from the United States following negotiations and struggles to attract global data centers due to a renewable energy shortage continue to hinder industrial competitiveness. Data center investments favor regions with abundant, low-cost renewable energy, and South Korea risks missing out due to the lack of readily available clean energy.

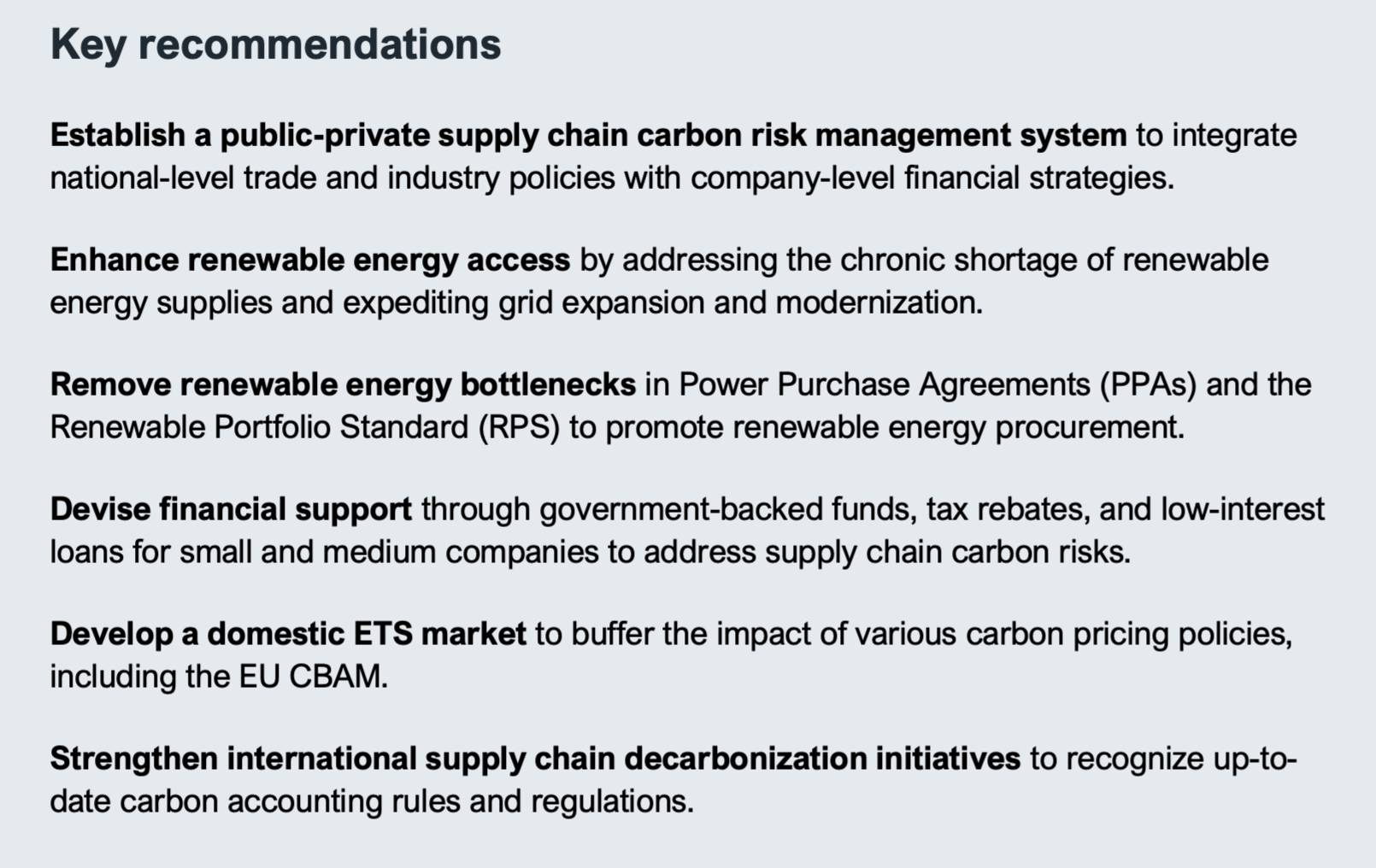

IEEFA recommends measures to address these supply chain carbon risks and bolster the competitiveness of South Korea’s tech industry, including the semiconductor sector and AI data centers.

2025 Sustainability Report. 27 June 2025. Page 77 and 79.

2024 Amazon Sustainability Report. July 2025.

Original Story at ieefa.org